What is a Health Savings Account (HSA)?

A Health Savings Account is a savings account that can be used in a variety of ways, primarily to pay for medical expenses. Account features include:

- Savings tool with investment earnings

- Flexibility to pay current qualified medical expenses or save for future needs

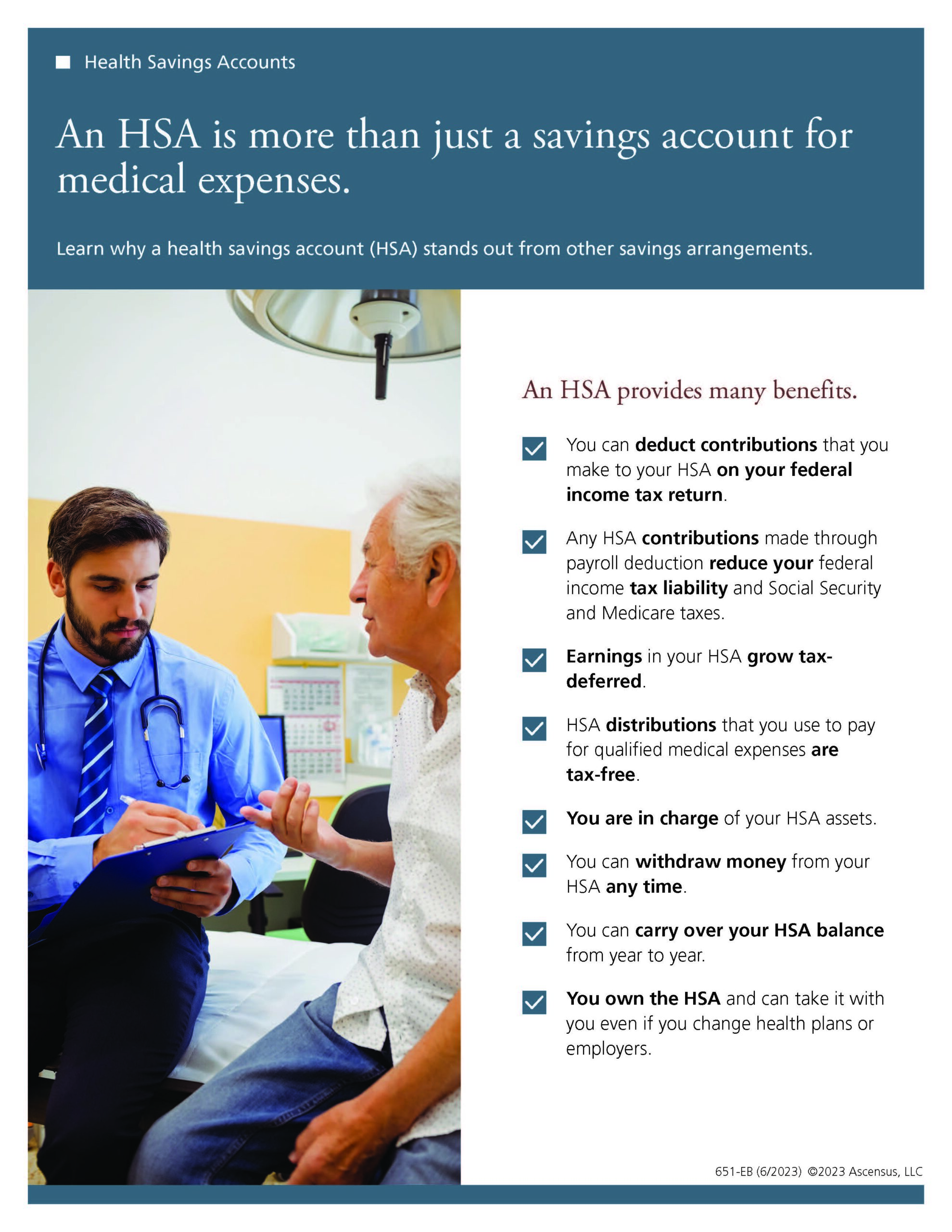

- Tax-deductible contributions

- Tax-deferred earnings

- Tax-free distributions if used within guidelines

Who can have an HSA?

An adult who is covered by a High Deductible Health Plan insurance policy, is not covered by another health plan (with limited exceptions), not enrolled in Medicare and cannot be claimed on another person’s tax return.

How can I use my HSA funds?

The money in your Health Savings Account can be withdrawn tax-free if used to pay qualified medical expenses as permitted under federal law. This includes most medical, dental, and vision care. While health insurance premiums generally are not included, the premiums paid for qualified long-term care insurance, health insurance when unemployed, health insurance under COBRA continuing coverage, and certain health insurance premiums after age 65 are included.

Funds in your Health Savings account can be used to pay medical expenses for you, your spouse and dependents- even if they are not covered by the High Deductible Health Plan (HDHP).

Health Savings Account funds can be used after your retirement for any reason! Just keep in mind that HSA distributions not used for qualified medical expenses are subject to ordinary income tax.

If the funds are used for non-qualified medical expenses before age 65, a 20% IRS tax penalty applies unless due to death or disability.

How can I invest the balance in my HSA account?

The funds that will accumulate in your Health Savings account earn tax-free dividends! You may take advantage of this by opting to invest in the Health Savings Account CDs offered at the credit union.

What happens to my HSA when I can no longer contribute?

You may continue to use the funds for medical expenses, or if over 65 or disabled, the funds can be used for any reason — and will be subject to ordinary income tax.

What if I change jobs?

If you remain under coverage of a High Deductible Health Plan, you don’t have to change anything. You are the owner of your HSA and can continue to contribute or access the funds as needed. If no longer covered under an HDHP, simply cease contributions until you become eligible. You can still use funds to pay for qualified medical expenses even if you can no longer contribute.

Do I have to use the funds in my account before the end of the year?

No — that is one of the many advantages of a Health Savings Account. You can invest and grow your balance perpetually.

Is there a limit on how much I can deposit into my HSA?

The IRS sets limits annually, please verify the contribution limit every year to ensure you are within these guidelines.

HSA contributions are generally tax deductible. You have until your tax return due date (usually April 15) to fund your HSA.

How can I access the funds in my HSA?

Beacon Credit Union offers a variety of options for account access.

- Free online banking

- Free online bill payment

- Free Visa Debit Card

- Free direct deposit/automatic withdrawal

- Checks are available for purchase

Can I designate another individual to access my HSA?

A spouse or another individual may be designated to make transactions for your Health Savings Account funds. This person would have all of the access options available to the account owner.

How can I transfer an existing HSA to Beacon Credit Union?

Simply complete an HSA application and direct transfer request form. The current HSA trustee/financial institution would send your account funds to Beacon Credit Union and you would be able to access your funds immediately upon arrival.